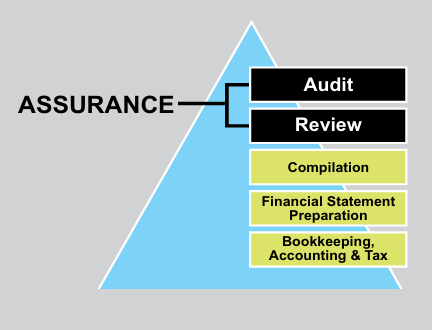

What Is the Difference Between an Audit, Review, and Compilation?

Audit vs review vs compilation are three financial statement services performed by CPAs that provide different levels of assurance on financial statements.

- Audit: Provides reasonable assurance through detailed testing and verification of financial information.

- Review: Provides limited assurance based on analytical procedures and inquiries.

- Compilation: Provides no assurance and involves presenting financial data in financial statement format.

These services vary in scope, procedures performed, and the level of confidence they provide to financial statement users.

Quick Comparison: Audit vs Review vs Compilation

The key differences between an audit, review, and compilation are summarized below:

| FEATURE | AUDIT | REVIEW | COMPILATION |

|---|---|---|---|

| Assurance Level | Reasonable Assurance | Limited Assurance | No Assurance |

| Procedures Performed | Testing transactions and confirmations | Analytical procedures and inquiries | Organizing financial information |

| Independence Required | Yes | Yes | Generally |

| Typical Users | Investors, regulators | Lenders, Nonprofit Boards | Internal Managers |

In general, audits provide the highest level of assurance because they involve detailed testing and verification of financial records. Reviews provide limited assurance through analytical procedures, while compilations present financial information without assurance.

Key Differences Between an Audit, Review, and Compilation

The main differences between these services relate to the level of assurance and procedures performed.

Key distinctions include:

- Level of assurance: Audits provide reasonable assurance, reviews provide limited assurance, and compilations provide no assurance.

- Procedures performed: Audits involve testing and verification, reviews involve analytical procedures, and compilations focus on presenting financial information.

- Cost and time: Audits typically require the most time and resources, while compilations are usually the fastest and least expensive.

- Purpose: Audits are often required for regulatory or investment purposes, while reviews and compilations are commonly used for financing or internal reporting.

Financial Statement Services Guide

If you’re comparing an audit, review, or compilation, you may find it helpful to review a detailed guide outlining these financial statement services and when they are typically used.

You can download our guide here:

Financial Statement Services Guide (PDF)

This guide explains the key differences between financial statement audits, reviews, and compilations and provides additional context for businesses and nonprofit organizations evaluating financial reporting requirements.

What Is a Financial Statement Audit?

A financial statement audit provides the highest level of assurance that financial statements are fairly presented according to the applicable accounting framework, such as U.S. GAAP.

During an audit, the CPA performs extensive procedures that may include:

- evaluating internal controls

- testing accounting transactions

- confirming balances with third parties

- reviewing supporting documentation

- performing analytical procedures

Following these procedures, the auditor issues an independent opinion on whether the financial statements are fairly presented.

Audits are commonly required when organizations:

- seek investment or financing

- must comply with regulatory reporting requirements

- receive government funding

- are preparing for acquisitions or major transactions

Many nonprofit organizations also face audit requirements based on funding thresholds.

What Is a Financial Statement Review?

A financial statement review provides limited assurance that the financial statements do not contain material misstatements.

Unlike an audit, a review does not involve testing transactions or confirming balances with third parties.

Instead, the CPA performs procedures such as:

- analytical comparisons of financial data

- inquiries with management

- evaluation of unusual relationships in financial statements

The CPA then issues a review report stating that they are not aware of any material modifications needed for the financial statements to conform with the applicable reporting framework.

Financial statement reviews are often requested when:

- lenders require limited assurance

- nonprofit boards seek financial oversight

- businesses want more credibility than internally prepared financial statements

Reviews provide a balance between credibility and efficiency, offering greater assurance than a compilation while requiring fewer procedures than an audit.

What Is a Compilation of Financial Statements?

A compilation engagement involves presenting financial information provided by management in the form of financial statements.

In a compilation engagement:

- the CPA does not verify financial information

- the CPA does not perform analytical procedures

- no assurance is provided on the financial statements

The CPA organizes financial data into financial statement format and issues a compilation report explaining that no assurance is provided.

Compiled financial statements are often used by:

- small businesses

- startups

- organizations seeking internally prepared financial reports

- companies needing structured financial statements without assurance

Although compilations provide the lowest level of assurance, they can help businesses maintain organized financial reporting.

Choosing the Right Financial Statement Service

Selecting the appropriate financial statement service depends on the needs of the organization and its stakeholders.

When an Audit Is Appropriate

An audit may be necessary when:

- investors require audited financial statements

- regulators mandate audited reporting

- nonprofits exceed funding thresholds requiring audits

- organizations are seeking significant financing

When a Review Is Appropriate

A financial statement review may be appropriate when:

- lenders request limited assurance

- management wants increased credibility

- organizations are preparing for future audits

When a Compilation Is Appropriate

A compilation may be appropriate when:

- financial statements are used primarily internally

- stakeholders do not require assurance

- a business needs professionally formatted financial statements

Understanding these distinctions helps organizations choose the appropriate level of financial reporting.

Why Financial Statement Services Matter

Reliable financial reporting supports transparency and credibility for businesses and nonprofits.

Proper financial statement services help organizations:

- strengthen trust with lenders and investors

- maintain regulatory compliance

- support financing and fundraising efforts

- improve financial decision making

Working with an independent CPA ensures financial statements are prepared and evaluated according to professional accounting standards.

Frequently Asked Questions

An audit provides reasonable assurance through detailed testing and verification of financial information, while a review provides limited assurance based primarily on analytical procedures and inquiries.

A compilation is a financial statement service where a CPA organizes financial data into financial statement format without providing assurance on the information.

The appropriate service depends on the needs of lenders, investors, regulators, or management. Audits provide the highest assurance, reviews provide limited assurance, and compilations provide no assurance.

Some lenders require audited financial statements for large financing arrangements, while others may accept reviewed financial statements depending on the loan terms.

A financial statement review generally costs less than an audit because it involves fewer procedures. Reviews rely primarily on analytical procedures and management inquiries rather than detailed testing.

Understanding the difference between audit vs review vs compilation allows organizations to select the financial reporting service that best fits their regulatory requirements, financing needs, and internal reporting goals.

Each engagement provides a different level of assurance, and choosing the right option helps ensure financial information is presented clearly and credibly to stakeholders.

If you’re unsure whether your organization needs an audit, review, or compilation, our CPA team can help you determine the appropriate financial statement service based on your regulatory and financing requirements.